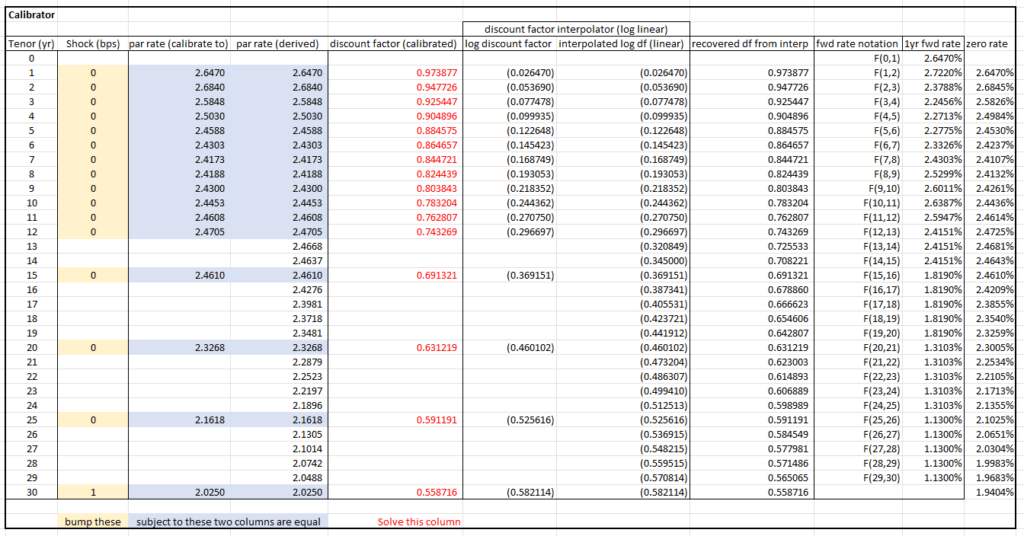

The attachment contains a toy RFR (e.g. SOFR, ESTR) )curve calibrator and a Libor-type pricer.

It is called a toy because the day count convention and effective/settlement date are not accurately considered. Also, the fine structure of the front end of the RFR curve (short tenors) is not handled. To handle front-end fine structure, short maturity instruments should be used as calibration instruments for example FRA (forward rate agreements). In this toy example, only par swap rates are used.

A key part of an interest rate calibrator is an optimizer or a solver (bootstrapping case only). In this toy example, Excel Solver is used. This is a widely available tool as long as you have Excel. See the Microsoft help page for how to turn on Solver: Load the Solver Add-in in Excel.

Note 1: The calibrator part is set up for a swap whose floating leg pay frequency is annual only, e.g., ESTR and SOFR, because the cashflows are evaluated out of 1-year forward rate. If you were to strip a Libor curve, you have to make the tenors granular enough to cover every payment (every quarter in the Libor case) and add more interpolation pillars.

Note 2: The RFR rate is compounded daily. The actual interest rate paid is a backward-looking backward rate. But it is still reasonable to use a forward rate to evaluate cashflows because any compounding format describes borrowing money for a certain period. The key variable that drives the whole curve is the discount factor, which could be equivalently expressed as forward rate, zero rate, etc.

: maturity of swaption

: maturity of swaption : tenor (maturity) of the underlying swap

: tenor (maturity) of the underlying swap : risk neutral measure

: risk neutral measure : annuity or annuity measure where annuity matches the floating leg pay frequency of the underlying swap

: annuity or annuity measure where annuity matches the floating leg pay frequency of the underlying swap : strike

: strike : discount factor from

: discount factor from  to

to

: par swap rate for a swap contract from

: par swap rate for a swap contract from  seen at

seen at  . We define a short-hand

. We define a short-hand  when there is no confusion.

when there is no confusion. : conditional expectation on

: conditional expectation on  for filtration

for filtration

: present value of something.

: present value of something.  : value of something at time

: value of something at time ![\[\small \begin{aligned} PV_{\mbox{payer}} =& \mathbb{E}_0^{\mathbb{Q}}\left[\left(V_{\mbox{float}}(\hat{T})-V_{\mbox{fixed}}(\hat{T})\right)^+P(0,\hat{T})\right] \\ =& \mathbb{E}_0^{\mathbb{Q}}\left[ \left(S_{\hat{T}}(\hat{T},\hat{T}+\Delta)A(\hat{T})-KA(\hat{T})\right)^+P(0,\hat{T})\right] \\ = & A(0) \mathbb{E}^{A}_{0} \left[\left(S_{\hat{T}}(\hat{T},\hat{T}+\Delta) - K\right)^+\right] \end{aligned}\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-46b8968ad668b901d385cf47984bfdcb_l3.png "Rendered by QuickLaTeX.com")

![\[\small \textrm{d} S_t = \sigma \textrm{d} W_t,\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-2dfbc9dc5a97161a82d4aa617124459e_l3.png "Rendered by QuickLaTeX.com")

is a standard Brownian motion under annuity measure and

is a standard Brownian motion under annuity measure and  is constant.

is constant. a normal distribution, we have

a normal distribution, we have ![\[\small S_{\hat{T}} \sim \mathcal{N}(S_0, \sigma\sqrt{\hat{T}}).\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-6ae89b3e67ab61f13258710b5995cea5_l3.png "Rendered by QuickLaTeX.com")

![\[\small \begin{aligned} & \mathbb{E}^{A}_{0} \left[\left(S_{\hat{T}} - K\right)^+\right] \\ = & \int_{K}^{+\infty} (x-K) \frac{1}{\sigma \sqrt{2\pi\hat{T}}} e^{-\frac{(x-S_0)^2}{2\sigma^2\hat{T}}} \textrm{d} x \\ = & \sigma \sqrt{\hat{T}} \cdot \varphi (d_1) + (S_0 - K) \cdot \Phi(d_1) \end{aligned} ,\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-eb1476fe039617fd4d4d8a91e72ba15f_l3.png "Rendered by QuickLaTeX.com")

is the probability density function of the standard Gaussian distribution

is the probability density function of the standard Gaussian distribution is the cumulative density function of the standard Gaussian distribution

is the cumulative density function of the standard Gaussian distribution

![\[\small PV_{\mbox{payer}} = A(0) \left[\sigma \sqrt{\hat{T}} \cdot \varphi (d_1) + (S_0 - K) \cdot \Phi(d_1) \right]\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-4f7a6fbf03ce4e29de01b29e13301587_l3.png "Rendered by QuickLaTeX.com")

![\[\small \mbox{Vega} =\hat{T}} \sigma \mbox{Gamma}\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-9ac2e214d7f81af6728151e809b678ce_l3.png "Rendered by QuickLaTeX.com")

depends on discounting curve, but one can approximate it by tenor (

depends on discounting curve, but one can approximate it by tenor (

. Let

. Let  be the discount factor discounting 1 dollar paid at

be the discount factor discounting 1 dollar paid at  to time

to time  . Let

. Let  be the floating rate reset date of the floating leg in a swap. For the case of LIBOR 3M,

be the floating rate reset date of the floating leg in a swap. For the case of LIBOR 3M,  if we assume the day count convention is that 3 months is

if we assume the day count convention is that 3 months is  of a year. Define

of a year. Define  .

.![[T_n, T_{n+1}]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-c38ca4c770f7df2a63709cab8cbf8b9b_l3.png "Rendered by QuickLaTeX.com") seen at time

seen at time  . Then,

. Then, ![\[L_n(t,T) := \frac{1}{\alpha_n}\left(\frac{P(t,T_n)}{P(t,T_{n+1})}-1\right).\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-710acd1c13e800ebe9c8ff62e2b5e6c6_l3.png "Rendered by QuickLaTeX.com")

![\[1+\alpha_nL_n(t) = \frac{1}{P(T_n, T_{n+1})} = \frac{P(t,T_n)}{P(t,T_{n+1})}.\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-65459fdd552215c13c4c5b2d1d781cf2_l3.png "Rendered by QuickLaTeX.com")

![\[\begin{aligned}f(t,T)&=\lim_{\delta\rightarrow 0}\frac{1}{\delta}\left(\frac{P(t,T)}{P(t,T+\delta)}-1\right) \\ & = -\frac{\partial \log P(t,T)}{\partial T}\end{aligned}.\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-b5a0732f224c579d77f26db98449ca36_l3.png "Rendered by QuickLaTeX.com")

is an instantaneous interest rate such that if

is an instantaneous interest rate such that if  is deterministic

is deterministic![\[P(t,T) = e^{-\int_t^Tr(s)\textnormal{d}s}.\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-8b1f27ef67480d96e4eb9834a87c4d7d_l3.png "Rendered by QuickLaTeX.com")

![\[P(t,T) = \mathbf{E}\left[e^{-\int_t^Tr(s)\textnormal{d}s}|\mathcal{F}_t\right].\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-3621ee3b252f8e851fcbe1952f5af0c4_l3.png "Rendered by QuickLaTeX.com")

by the forward par swap rate on tenor

by the forward par swap rate on tenor ![[T_n, T_{N+1}]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-c4c99c5d89ad46056f2b9f853db0b6bb_l3.png "Rendered by QuickLaTeX.com") . Suppose the pay frequency of the fixed leg is the same as the floating leg (otherwise redefine the below annuity as one that matches the fixed leg pay frequency). Let

. Suppose the pay frequency of the fixed leg is the same as the floating leg (otherwise redefine the below annuity as one that matches the fixed leg pay frequency). Let  represents the present value of annuity, i.e.,

represents the present value of annuity, i.e.,![\[A_n(t) = \sum_{k=n+1}^{N+1} \alpha_{k-1}P(t,T_k).\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-b2ec3de0caee6a648cf582e5f4fa3a7f_l3.png "Rendered by QuickLaTeX.com")

![\[PV_{\mbox{fix}} = S_n(t)A_n(t)\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-5283d1b33e7286eb516f7047641d08a0_l3.png "Rendered by QuickLaTeX.com")

![\[\begin{aligned}& PV_{\mbox{float}} \\ = & \sum_{k=n}^N L_k(t)\alpha_k P(t,T_{k+1}) \\ =& \sum_{k=n}^N \frac{1}{\alpha_k}\left(\frac{P(t,T_k)}{P(t,T_{k+1})}-1\right) \alpha_k P(t,T_{k+1}) \\ =& \sum_{k=n}^N \left(P(t,T_k) - P(t,T_{k+1})\right) \\ =& P(t,T_n) - P(t,T_{N+1}) \end{aligned}\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-faa76195580877c1bc9e022c4ab6f116_l3.png "Rendered by QuickLaTeX.com")

, we have that

, we have that![\[S_n(t) = \frac{P(t,T_n) - P(t,T_{N+1})}{A_n(t)}.\]](https://sisitang0.com/wp-content/ql-cache/quicklatex.com-f2e8c8d6e477fe4843b6a420cefb0fde_l3.png "Rendered by QuickLaTeX.com")